The insurance industry is embracing AI, and it's poised to significantly impact the way we get insured. While some aspects, like self-driving cars, will necessitate entirely new insurance solutions, others leverage existing technology. Blockchain technology can fight fraud and streamline claims processing, while wearables and smart home devices can unlock personalized premiums. AI chatbots are already being used to answer basic questions, and a single policy for all your coverage needs might be the future, but it remains to be seen how widely adopted this will be.

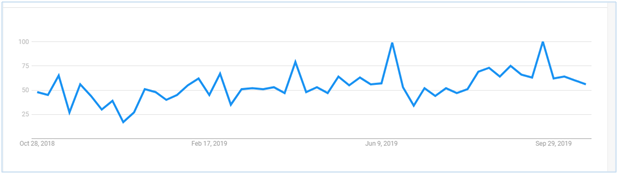

Typically, as an industry, insurance is not at the forefront of innovation and technology. Regulation and compliance rules in a risk-averse sector that deals with many legacy systems do not equate to forward-thinking. However, in recent times, substantial interest in the term “Insurtech,” according to Google Trends, suggest things are changing. Insurtech uses innovation and technology to gain savings and efficiency in the current insurance industry framework. Firms in the insurance sector might be slow to make changes, but the evidence shows they want to. Note, we are offering 2019 figures below as 2020 numbers are disproportionate following the Covid-19 pandemic.

Interest over time in the term “Insurtech” in the US 2019 – source: Google Trends

The trend above is a 30% increase between 2018 and 2019 alone.

At the start of 2020, artificial intelligence (AI) is infiltrating the insurance industry as firms realize the benefits of deploying the technology. In this post, we look at AI trends within the insurance sector and how they will influence the industry for the remainder of 2020.

What is AI?

Sometimes it is difficult to understand what the state of AI is today, with so much hype and myth surrounding the term and its applications. AI helps machines demonstrate intelligence through data. Computers gather data from their surroundings, using it to make decisions, and continually learning from their actions. The aim is for machines to develop a similar contextual understanding of the human brain (another field called neural networks).

AI applications that exist today are narrow forms of technology. That is to say; they operate from sets of rules that a human defines, rather than having their own type of consciousness. Movies tend to lead us to believe AI is synonymous with robotics. While robots can offer solutions, they are not typical of 21st-century AI yet. Talking to our smartphones, searching on Google, Amazon product recommendations, and Netflix telling us what to watch are common daily uses that have revolutionized everyday life.

In the insurance sector, independently learning machines have various areas where they could be game-changing and are already having a sizeable impact.

Autonomous Vehicles

Industry experts proclaim that autonomous or driverless vehicles are on the horizon. However, in the last decade, the plans have never come to fruition for reasons like data privacy, sharing, and latency. In 2020, with more tests going on every day and introducing technology like 5G enhancing connectivity, we are slowly starting to see these vehicles moving into society. Autonomous cars could fundamentally change the face of motor insurance.

One question that arises is a liability at the time of a claim. For example, if an accident occurs today, a human driver is at fault, and the insurance company can deal with it accordingly. However, with a self-driving car, where does the responsibility lie, and who does that sit within terms of insurance?

Companies including Google, Volvo, and Mercedes have already said they will accept liability for any accidents involving their cars. However,Tesla says they intend to extend an insurance plan to all owners of their products. Standardizing insurance offerings for autonomous vehicles will take time when technology is still too immature to create the right products.

Ridesharing presents a further challenge for the motor insurance vertical.Companies like Uber and Lyft are looking to a “ridesharing insurance” over typical motor cover, given the unique circumstances of their services. Insurers need to look at ways to bridge the gap between traditionally motor cover and ridesharing, to serve the rising customer demand for such products.

Blockchain Technology

People tend to associate blockchain with cryptocurrencies such as Bitcoin, Ethereum, and Ripple. Bitcoin and blockchain are sometimes used interchangeably, but the blockchain is the technology on which bitcoin resides.Insurance firms are now integrating blockchain technology into existing frameworks as they seek to avoid losses, mitigate fraud, and remove manual business processes.

A blockchain is a centralized ledger where it is impossible to edit or delete a transaction once verified by all parties. In other words, it is a giant audit trail of transactions that anyone with access to the blockchain can view as applicable. Blockchain is the perfect technology for understanding false claims, fraud, or money-laundering as every interaction needs verification to be part of the shared ledger. Insurance companies can benefit from reducing loss ratios, while their customers can have faster claims settlement processes, without length forms and admin.

A blockchain starts as soon as underwriting the insurance policy begins. You can think of insurance just like any contract. People pay a premium that an underwriter covers for the terms laid out by them, i.e., the contract. In residential insurance, this might be for if somebody has a break-in, they are insured for their contents, assuming the doors have adequate security features. If a customer needs to claim, they notify the underwriter, it enters the blockchain, and if it meets the terms of the contract, they may get an instant payout. Lemonade, in the US, are pioneers of such technology.

Blockchain provides the insurer with a single source of truth that can automate many of their manual processes. Customers get a better experience, and data is more accurate than legacy insurance systems.

Personalizing Insurance Premiums

Personalization is now more of an expectation of consumers, with big tech companies like Google, Facebook, and Amazon, making it a standard within retail and social media. Customers want to see products that relate to them, rather than generic services typically part of an insurance offering. The insurance industry needs to adapt, treating customers as individuals how they underwrite and price policies.

If insurers are to deliver a personalized premium, they need data and lots of it. An Accenture report shows that 77% of customers are willing to provide data if it means they benefit from cheaper premiums. The same study shows that only 22% of insurers have such services at the time of writing, missing out on the opportunity.

Smart home technology is now part of everyday life, as voice-activated devices like Alexa and Google Home become more advanced and commonplace. Companies like Neos now offer connected home insurance. They provide customers with the latest technology, such as pipe sensors, cameras, and smoke alarms, to reduce or ideally eradicate claims situations. For example, a valve on water pipes can detect irregular flow and notify the occupant before a flood occurs.

If customers fill their homes with smart equipment that reduces claims, insurers can reduce premiums, safe knowing that the customer home is better protected.

In health insurance, companies are beginning to invest in wearable technology to understand personal health data. For example, if a customer exercises daily, they may benefit from a premium reduction over somebody that doe not take such good care of themselves.

Motor insurers are using telematics technology to understand driver behavior. Drivers receive premiums depending on their driving habits, via a device in their car. Metrics will include their speed, the way drivers brake, and their handling of corners. Each of the metrics contributes to accidents, meaning positive data reduces claims, and customers deserve better premiums.

Enhancing the customer experience

AI is already enhancing customer experiences in insurance. There are two key areas where this is prevalent.

Settling claims

A typical insurance claim process can be lengthy. Customers and staff need to fill in much paperwork; there can be several calls, visits, and audits. AI can solve many of the problems associated with the claims process.

Self-service is key to the automation of claims settlement, right through from notification of loss to payment. Take a product like travel insurance during the Covid-19 pandemic. Due to restrictions and quarantine situations, many customers were left having to cancel holidays and, therefore, their insurance. Some airlines canceled up to a quarter of flights at the start of the pandemic.

Flight information is readily available online through airline websites. A self-service AI platform can scrape this information and relate it to the insurance contract. For example, when taking out insurance, the customer can log their flight number, having it automatically checked for delays and cancellations. In the event of a cancellation, claim payout is instant, without the need for human intervention. Claims settlement is the perfect use case for blockchain technology.

Customer Service Chatbots

Call center staff are an expensive resource. While they are generally experts in their field, much of their time is taken, answering basic questions or handling repetitive tasks. Chatbots are the solution to the problem.

Conversational chatbots are now commonplace in most industries. They are programs that communicate with humans using a combination of AI and Big Data. In some cases, it is tough to differentiate between humans and robots because they are so well developed. Alexa, Siri, Cortana, and Google Home are all examples of chatbots, taking in commands and responding appropriately.

Within insurance, chatbots can answer standard customer queries, allowing human agents to be responsible for more complex cases. Customers can get a quick response without the need for a call or email, while staff benefit from not having to answer repetitive questions. For example, Next Insurance’s chatbot helps shoppers with the insurance buying process, while GEICO’s virtual assistant provides information on coverage, billing details, and documentation through a mobile app.

As the digital ecosystem continues to grow exponentially, customers are favoring new technology, and insurance firms need to keep up with the trend. There is an opportunity for insurance to deliver experiences, rather than just products, and it’s essential they make this happen.

Insuring a person, not a product

Within insurance, there is an emerging trend that looks to insure people, rather than just supplying them with products. The concept is in line with Open Banking that has started to be more accepted commercially since 2019. Instead of having several providers for motor, health, life, residential, travel, or pet insurance, customers have one product designed to suit them.

Underwriters will use data to understand everything about a customer, pulling the information into a single view. For example, John Smith is 35 years old, lives in Florida with his wife and two children. John does not smoke, one who exercises regularly has a dog and a cat, and travels abroad three times per year. John’s premium is $100 based on his personal risk.

AI platforms have the potential to revolutionize the industry altogether.

Summary

It is becoming crucial for insurance companies to understand how AI is changing the industry. The topics in this post are by no means exhaustive but show some of how sector incumbents are seeking to innovate and scale their business. In our future post, we will look at the insurer of 2030 and what they might look like as AI and Big Data become more firmly embedded into existing operating models.

Manish Garg is the co-founder and chief product officer of Skan.ai, a cognitive process discovery and operational intelligence platform.