The insurance industry is on the cusp of a major transformation driven by artificial intelligence. By 2030, AI will automate many tasks, potentially leading to faster quotes and a more streamlined claims process. However, the impact of AI on underwriting and claims processing is still under development. On the other hand, AI is expected to play a significant role in personalizing insurance policies, allowing for coverage tailored to your unique needs.

The insurance sector is transforming rapidly, thanks to advancements in computing power, technology, connectivity, and access to vast amounts of data. Throughout the 2020s, the pace of change will likely continue as industry incumbents, and consumers alike become accustomed to new ways of interacting with insurance products.

The penetration of existing devices like fitness trackers, home assistants, smartphones, and watches, is still increasing month-on-month, generating a mass of new data for the insurance sector. Underwriters can understand clients more deeply than ever before, and need to act, else risk stagnating behind the competition.

In this article, we look forward to 2030 and how cognitive technologies may shape the insurers of the future.

What are Cognitive Technologies?

Cognitive technology is a domain of computer science that aims to imitate the function of a human brain. The term is often used interchangeably with artificial intelligence (AI) and includes techniques like computer vision, natural language processing, data mining, and predictive analytics.

Within the insurance sector, cognitive automation replaces or augments human functions across sales, service, risk, underwriting, claims, and compliance. Machines now do facets such as making discoveries and decisions that only a human could once do. Examples include investigating fraud, assessing creditworthiness, and reviewing claim documents. You can read more about some of these applications in our previous post.

We’re not going to look at those applications in depth here, but instead, turn to 2030 and what the insurance sector might look like then.

How Big Tech is Influencing Cognitive Technology

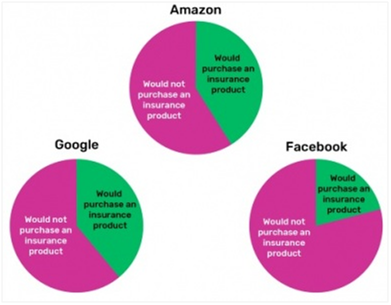

The likes of Amazon, Google, and Facebook have immense power when it comes to cognitive technology. A wealth of resources, data, and technology through the acquisition of startups puts them in a position where they could threaten the insurance industry. Amazon already works with JPMorgan Chase to help US employees find quality healthcare at a reasonable cost and have been active in the Indian insurance market.

Insurers need to prepare themselves for the next level of competition that the big tech companies can bring to the market. Amazon will likely offer cheaper rates, putting pressure on insurers, especially with the vast data asset that the tech firm owns. In the UK, 30% of people say they would buy insurance from Google, Amazon, or Facebook.

Source: Youtalk-insurance

To stay competitive, insurance companies will partner with startups that can spark innovation.

Manual Underwriting No Longer Exists

By 2030, the underwriting process will be automated using data. Machine learning and deep learning models will be sophisticated enough that there is no need for human intervention. If we consider that this is already starting to happen, with a decade more data in 2030, it would be surprising if full automation is not a reality.

For example, Cape Analytics supply insurance companies with a list of property attributes from a given postcode. The platform uses satellite images to gain risk details for the property. Insurers have an accurate inspection without the need for human agents or inspectors. By 2030, services like this will become the norm as insurance firms reduce costs and improve customer experience.

The unique selling point for insurers will be in how they use the data. The role of underwriting will change to one that is far more strategic, considering the way that they use different data points to generate pricing.

Processing Claims in Minutes with Cognitive Automation

The claims process is a significant pain point for consumers when it comes to insurance. The sheer amount of administration that goes into making and settling a claim can take weeks, if not months, to handle. There will be phone calls, emails, forms, documents, inspections, and reports to complete. When we reach 2030, computing power, network infrastructures, and connectivity will be sufficient enough to settle claims at speed.

Insurance companies like Lemonade already use cognitive technology in the claims process and evidence the potential to payout within a few minutes. Tractable offers software for claims process automation using computer vision, with consumers uploading an image to receive back an estimate of their payout. While the software is not yet mainstream, the concept is one that consumers demand and will form part of the future of insurance.

The success of automating claims relies on 5G connectivity and the Internet of Things (IoT). IoT sensors need to be powerful enough to replace manual methods, while 5G can transfer data without latency. For example, if someone has a car accident, the video can automatically stream straight to the insurance company. Afterward, computer vision translates it into a description of the loss, ready for payout.

Motor insurance is one vertical that could drastically change with cognitive automation. If autonomous vehicles get enough backing and development to become commercialized, motor insurance in its current form will not work. In 2030, we will need a new kind of insurance that suits the driverless vehicle market.

Humans can spend time working on complex queries rather than claims administration, which a machine can handle.

Insuring the Individual

The 21st-century consumer demands a personal experience. In 2020, there is still a need to buy multiple products for different aspects of your life. For example, if John owns a house, two cars, has a dog, two children, and travels three times a year, he needs to purchase residential, motor, pet, life, and travel insurance all separately.

A trend that we may start to see is cover for the individual as a vertical in its own right. The reason is two-fold. Firstly, buying multiple products incurs several fees for the customers, creates lots of documentation, and products that they don’t need all the time. Second, consumers want a personalized product, which they now expect from the experience they get in the retail and social world.

John would go to an insurer, tell them he has a home, two cars, a dog, two children, and travels three times per year. The cover they offer is for John as an individual, mitigating the need for many different products.

The challenge will be in underwriting such a product efficiently, but as insurers gather more data, the “insuring the individual” product is a trend we will see moving towards 2030.

Automate the Value Chain

Through data, by 2030, insurers will know enough about their customers, not even to be involved in the purchasing process. AI algorithms will produce accurate risk profiles in real-time, allowing the purchase of insurance products to complete in minutes, or even seconds. There are some early adopters of these services, such as Aviva, who rolled out no questions home insurance in 2017. As data becomes more available via IoT devices, and algorithms mature, quote automation will become a standard feature of insurance.

Blockchain will finally embed itself within the insurance value chain. Smart contracts will enable the instant authorization of payments, reduce the risk of fraud, and support claims settlement. Insurers will be able to act proactively using blockchain technology.

Personal assistants (chatbots) will form service interactions, reducing the need for large call centers and human agents handling repetitive queries.

Automating acquisition, service, underwriting, and claims will lead to the digitized insurance industry.

Pay-As-You-Go Insurance

A long-standing problem with insurance is that customers pay a monthly or annual premium for a product they may never use. Insurers are already beginning to offer pay-as-you-go insurance as an alternative to traditional products. Using cognitive technologies, insurers can gain a more accurate view of the customer, to personalize what they pay, rather than offering a one size fits all price.

Zego, for example, provides pay-as-you-go cover for delivery drivers and couriers. Premiums are based on how often you use the car, rather than a set monthly fee. Customers can get a fairer deal if they drive less frequently and do so safely. Data from telematics sensors helps insurers gather enough data to perform automated underwriting.

Travel insurance will become a pay-as-you-go product. Typically, customers purchase travel insurance annually or for a specific trip. A pay-as-you-go product like Revolut uses geolocation to track its customers via a mobile app. The app detects when someone leaves and returns to the country, switching cover on and off automatically. Customers benefit from an enhanced experience, while insurers can more accurately underwrite risk depending on the precise location of a policyholder.

Pay-as-you-go solves the issues associated with insurance premiums, and we expect this to be a continually growing market leading up to 2030.

Summary

AI and its applications are already impacting the insurance industry. As we move towards 2030, the value chain will continue to transform through AI and new cognitive technologies. Insurers should prepare themselves by integrating cognitive automation, deep learning, and data as standard parts of their ecosystem. Although we can’t tell exactly what the next decade holds, inevitably, those fields will all have a large role to play. A clear data strategy, infrastructure plan, and the right talent will put incumbent insurance firms in a strong competitive position come 2030.

Learn more about automation opportunities across the insurance value chain or subscribe to the Skan blog below.

Avinash Misra is the co-founder and CEO of Skan.AI.